Family Law

What is financial settlement: a compassionate UK guide

When your marriage ends, the question of how to divide everything you’ve built together can feel overwhelming. Financial settlement is the legal process that determines who gets what, from the family home to pensions and savings. It’s designed to be fair, but understanding what ‘fair’ actually means in law can ease much of the anxiety. This guide explains the principles behind financial settlements in the UK, the process you’ll follow, and how courts balance competing needs to reach outcomes that protect both parties. Whether you’re just starting to consider separation or already negotiating terms, you’ll find clarity on what to expect and how to prepare.

Table of Contents

- Key takeaways

- What does a financial settlement mean in UK divorce?

- Key legal principles guiding financial settlements

- The financial settlement process: from disclosure to resolution

- Balancing needs and sharing: navigating difficult decisions

- How Signature Law can support your financial settlement journey

- What are common questions about financial settlements?

Key Takeaways

| Point | Details |

|---|---|

| Full disclosure required | All assets, debts, income and outgoings must be disclosed on Form E to allow informed negotiation. |

| Paths to agreement | Mediation, collaborative law, solicitor led negotiation, and court proceedings are the main routes to finalising a settlement. |

| Needs come first | The court prioritises sufficient resources for housing and income, with children’s needs given priority. |

| Most settle before court | Around 70 to 90 per cent of cases settle before the final hearing, avoiding court where possible. |

What does a financial settlement mean in UK divorce?

A financial settlement is the legally binding agreement that resolves all money and property matters when your marriage or civil partnership ends. It covers everything from the family home and savings accounts to pensions, investments, and even future maintenance payments. Without this formal agreement, either party could return to court years later seeking a share of assets, which is why finalising your financial settlements in divorce UK provides essential closure.

The foundation of any settlement is complete financial disclosure. Both parties must complete Form E, a detailed document listing all assets, debts, income, and outgoings. This transparency allows you to negotiate from an informed position. You’ll declare bank accounts, property values, pension statements, business interests, and even items like valuable jewellery or vehicles. Hiding assets or providing incomplete information can result in the court setting aside any agreement reached, so honesty is not just ethical but legally necessary.

Once disclosure is complete, you have several paths to agreement:

- Mediation, where a neutral third party helps you negotiate directly

- Collaborative law, where both parties and their solicitors commit to reaching agreement without court

- Solicitor-led negotiation through correspondence

- Court proceedings if negotiation fails

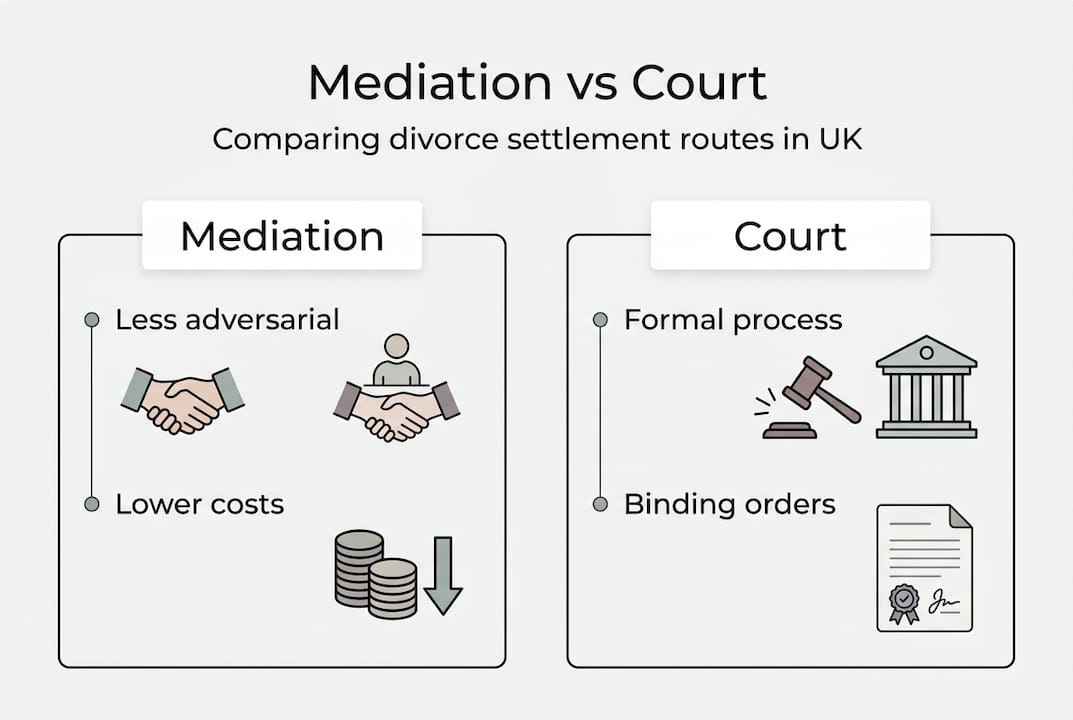

Most couples prefer to avoid court. The process involves full financial disclosure, negotiation, mediation, or court stages including First Appointment, Financial Dispute Resolution, and Final Hearing, yet 70-90% settle before the final stage. Court is expensive, stressful, and puts the decision in a judge’s hands rather than your own. If you do proceed to court, the First Appointment focuses on identifying issues and narrowing disputes. The Financial Dispute Resolution hearing is a settlement meeting where a judge gives an indication of the likely outcome. Only if these fail does a case proceed to a Final Hearing, where the judge makes a binding decision.

Emotionally, reaching a financial settlement marks a turning point. It allows you to move forward with certainty about your financial future, plan new housing arrangements, and close the legal chapter of your marriage. The process may feel daunting, but understanding each stage helps you approach it with confidence rather than fear.

Key legal principles guiding financial settlements

UK courts don’t apply a rigid formula to divide assets. Instead, judges consider three core principles: needs, sharing, and compensation. Understanding how these work together helps you anticipate what a court might order and negotiate more effectively.

Needs always come first. The court must ensure both parties have sufficient resources to meet their essential requirements, particularly housing and income. If you have children, their needs take priority. The court considers what accommodation is necessary for each household, whether one party requires retraining to re-enter employment, and how long maintenance payments might be needed. Needs are assessed generously where assets allow, but realistically where they don’t. In modest asset cases, needs often consume everything available, leaving nothing for sharing principles to apply.

Sharing applies to matrimonial assets once needs are met. Matrimonial assets include everything acquired during the marriage through joint efforts: the family home, savings built up together, pensions accrued during the relationship. The starting point is equal division, reflecting the principle that marriage is a partnership of equals. However, this equal split applies only after needs are satisfied and typically excludes non-matrimonial property.

Compensation addresses situations where one party sacrificed career prospects or earning capacity for the family’s benefit. This principle is rarely invoked because maintenance payments usually address ongoing financial imbalances. Compensation might apply if one spouse gave up a high-flying career to raise children while the other’s career flourished, creating a significant and enduring disparity that maintenance alone cannot remedy.

Principles prioritise needs for housing and income, then equal sharing of matrimonial assets after needs are met, with compensation rare and applied for career sacrifice. Non-matrimonial assets such as inheritances, gifts, and property owned before marriage are often ring-fenced unless needs require otherwise, following cases like Standish v Standish.

How courts apply these principles in practice:

- Identify all assets and categorise them as matrimonial or non-matrimonial

- Calculate each party’s reasonable needs, prioritising children’s welfare

- Allocate assets to meet those needs first

- Apply equal sharing to any surplus matrimonial assets

- Consider whether non-matrimonial assets must be invaded to meet needs

- Assess whether compensation is warranted for career sacrifice

| Principle | Focus | When it applies |

|---|---|---|

| Needs | Essential housing, income, children’s welfare | Always, takes priority |

| Sharing | Equal division of matrimonial assets | After needs met, surplus assets |

| Compensation | Redress for career sacrifice | Rare, significant disparity cases |

Pro Tip: If you received an inheritance or owned property before marriage, gather clear documentation showing the source and timing of these assets. Courts are more likely to protect non-matrimonial wealth when you can demonstrate it remained separate from family finances. Evidence matters when arguing for ring-fencing.

The financial settlement process: from disclosure to resolution

Navigating the settlement process becomes less intimidating when you understand each stage. The journey typically unfolds in three main phases, though many cases resolve before reaching court.

Step one is complete financial disclosure. You and your spouse each complete Form E, a comprehensive 30-page document detailing every aspect of your financial life. You’ll attach 12 months of bank statements, mortgage statements, pension valuations, business accounts if applicable, and valuations of property and significant assets. This stage often takes several weeks as you gather documents and verify figures. Your solicitor will review the form before submission to ensure accuracy and completeness. Once exchanged, both parties can ask questions about unclear entries or request additional documentation.

Step two involves negotiation. Most couples attempt to reach agreement through one of several methods:

- Mediation sessions where you discuss options with a neutral mediator

- Solicitor-led correspondence proposing and counter-proposing terms

- Collaborative law meetings with both parties and solicitors present

- Round-table meetings bringing everyone together to negotiate directly

This phase requires patience and flexibility. You’ll likely exchange multiple proposals before finding common ground. Your solicitor will advise on whether offers are reasonable given the legal principles and your circumstances. The process involves full financial disclosure, negotiation, mediation, or court stages with 70-90% settling out of court, so persistence in negotiation often pays off.

Step three is court involvement if negotiation fails. The court process has defined stages:

- First Appointment: A preliminary hearing where the judge identifies issues, sets timetables, and may order valuations or expert reports

- Financial Dispute Resolution: A settlement-focused hearing where the judge gives a non-binding indication of the likely outcome to encourage agreement

- Final Hearing: A full trial where both parties give evidence and the judge makes a binding decision

Documents and evidence required at each stage include updated asset valuations, income evidence, expert reports on pensions or businesses, and witness statements explaining your position. The steps in family law proceedings provide structure and deadlines that keep cases moving forward.

Pro Tip: Engage a solicitor as early as possible, ideally before completing Form E. Errors or omissions in disclosure can undermine your credibility and delay proceedings. Professional guidance ensures you present your financial position clearly and compellingly from the outset.

Mediation offers significant advantages over court. It’s less adversarial, allowing you to maintain a working relationship with your ex-partner, which matters especially when you’re co-parenting. It’s faster, often reaching resolution in weeks rather than months. It’s cheaper, with mediation sessions costing a fraction of court hearings. And it gives you control, allowing you to craft creative solutions that a judge might not order. Even if mediation doesn’t resolve everything, it often narrows disputes and reduces court time needed.

Balancing needs and sharing: navigating difficult decisions

The tension between needs and sharing creates some of the most challenging debates in financial settlements. Should surplus assets be divided equally even if one party brought significantly more wealth into the marriage? How do you balance fair recognition of contributions against practical housing requirements? These questions don’t have simple answers, and courts must weigh competing principles case by case.

The needs-based approach prioritises ensuring both parties can live adequately post-divorce. It recognises that marriage creates mutual obligations that don’t vanish instantly upon separation. If you’ve been married for decades and one spouse sacrificed career for family, needs-based reasoning ensures that person isn’t left destitute. Critics argue this can feel unfair to the higher earner, who may see a large portion of assets awarded to meet the other’s needs even in shorter marriages.

The sharing approach treats marriage as an equal partnership where both contributions, financial and domestic, deserve equal recognition. It reflects modern attitudes that homemaking and childcare are as valuable as paid employment. Sharing applies most clearly to assets built during the marriage. However, in cases where needs consume all available assets, sharing never comes into play, which some see as undermining the partnership principle.

Common challenges that arise include:

- Protecting inheritances received during a long marriage when the other spouse has significant needs

- Dividing assets fairly when one party owned substantial pre-marital property

- Balancing business interests built by one spouse against the other’s domestic contributions

- Determining how much weight to give short marriage duration versus needs created during that time

Contrasting views on needs versus sharing reflect ongoing debate among legal experts, with fairness nuanced after Standish, which better protects non-matrimonial assets in surplus cases. As one family law specialist observed:

“The Standish decision represents a recalibration towards recognising the source of wealth. Non-matrimonial property now receives greater protection where assets exceed both parties’ needs, but courts retain discretion to invade those assets when necessary to achieve fairness.”

In practice, courts apply these principles flexibly. In cases with surplus assets, non-matrimonial wealth is more likely to be ring-fenced. A spouse who inherited £500,000 late in a marriage may retain most of it if the matrimonial assets suffice to meet both parties’ needs. Conversely, in modest asset cases, the court may use inheritance to ensure adequate housing for both households, prioritising needs over source of funds.

Understanding types of divorce settlements UK courts can order helps you anticipate outcomes. Clean break orders sever financial ties completely, with no ongoing maintenance. Maintenance orders provide regular payments for a spouse who cannot immediately become self-sufficient. Pension sharing orders divide retirement assets, recognising these often represent the largest asset after the home. Each type serves different circumstances, and your settlement may combine several elements.

When negotiating, communicate clearly with your solicitor about your priorities. If protecting an inheritance matters deeply, explain why and provide evidence of its separate nature. If you need ongoing maintenance to retrain for employment, outline a realistic plan and timeline. Courts appreciate parties who approach settlement constructively rather than rigidly defending positions. Flexibility often leads to better outcomes than aggressive litigation.

How Signature Law can support your financial settlement journey

Navigating financial settlements requires both legal expertise and genuine compassion for what you’re experiencing. At Signature Law, we understand that behind every financial disclosure form and settlement proposal is a person facing one of life’s most difficult transitions. Our family law UK impact reflects our commitment to supporting clients through these challenges with clarity, professionalism, and empathy.

Our experienced financial settlement solicitors guide you through every stage, from initial disclosure to final agreement. We explain complex legal principles in plain language, help you understand what outcomes are realistic, and negotiate assertively on your behalf. For clients in London and across the UK, our family law solicitors London team provides accessible, personalised advice tailored to your unique circumstances. Contact us today to discuss how we can support your financial settlement and help you move forward with confidence.

What are common questions about financial settlements?

What documents are needed for financial settlement?

You must complete Form E listing all assets, debts, income, and expenses. Attach 12 months of bank statements, mortgage statements, pension valuations, payslips, tax returns, property valuations, and business accounts if applicable. Your solicitor will guide you through gathering comprehensive documentation.

How long does the settlement process usually take in the UK?

Timelines vary significantly based on complexity and cooperation. Straightforward cases settled through mediation may resolve in three to six months. Cases requiring court involvement typically take 12 to 18 months from initial application to final order. Delays often stem from obtaining valuations or one party not engaging constructively.

Can I change a financial settlement after it’s finalised?

Once a court approves a financial settlement and issues a consent order, it’s binding and extremely difficult to change. You can only appeal or vary an order in exceptional circumstances, such as fraud, material non-disclosure, or a fundamental change in circumstances like serious illness. This is why getting the settlement right initially matters enormously.

Are mediation outcomes legally binding?

Mediation itself is not legally binding. Agreements reached in mediation must be formalised into a consent order approved by the court to become enforceable. Until the court seals the order, either party can withdraw from the agreement. Your solicitor will draft the consent order reflecting mediation terms and submit it for judicial approval.

How does legal aid work for financial settlement cases?

Legal aid for financial settlement matters is limited and means-tested. You generally qualify only if you’re a victim of domestic abuse and meet strict financial eligibility criteria. Most financial settlement cases are not covered by legal aid, though initial advice may be available. For detailed FAQ about family law proceedings including funding options, consult a specialist solicitor who can assess your situation.

Recommended

- Understanding Financial Settlement Agreements: A Comprehensive Guide to Divorce Financial Settlements in the UK

- Understanding Financial Settlement Agreements: A Comprehensive Guide for UK Divorce | Signature Law

- Role of Financial Settlements in UK Divorce: 70% Settled Out of Court | Signature Law

- Divorce Settlement Explained – Fair Outcomes in 2026 UK | Signature Law