Family Law

Estate planning guide UK: secure your family’s future in 2026

Every year, thousands of families face unnecessary legal disputes, frozen assets, and unexpected tax bills because estate planning was left too late or done poorly. Without proper preparation, your loved ones could spend months navigating probate courts, arguing over inheritances, or losing significant portions of your estate to avoidable taxes. This guide walks you through the essential steps to protect your assets, prepare legally sound documents, and ensure your family’s financial security under the latest UK laws and tax changes taking effect in 2026 and beyond.

Table of Contents

- Understanding Inheritance Tax Thresholds And Reliefs

- Making A Will That Protects Your Assets And Family

- Navigating The Probate Process Effectively In The Uk

- Estate Planning For Pension Pots And Digital Assets In 2026

- How Signature Law Can Support Your Estate Planning Journey

- Frequently Asked Questions About Estate Planning In The Uk

Key takeaways

| Point | Details |

|---|---|

| Frozen tax thresholds | Inheritance tax nil-rate bands remain at £325,000 and £175,000, pulling more middle-income families into the tax net as property values rise. |

| Agricultural relief caps | From April 2026, full agricultural and business property relief will be capped at £1 million, with only 50% relief available thereafter. |

| Pension tax changes | Pension pots and death-in-service benefits will become subject to inheritance tax from April 2027, requiring urgent beneficiary reviews. |

| Digital asset planning | Modern wills must account for digital assets like cryptocurrency, social media accounts, and online banking to avoid access complications. |

| Rising probate disputes | Caveat applications challenging wills increased 79% since 2010, highlighting the critical need for legally robust estate documents. |

Understanding inheritance tax thresholds and reliefs

Inheritance tax planning starts with knowing your exposure. The Inheritance Tax nil-rate band (£325,000) and residence nil-rate band (£175,000) remain frozen, pulling more middle-class families into the IHT net as property values continue rising across the UK. If your estate exceeds these combined thresholds, everything above faces a 40% tax charge unless you qualify for specific reliefs.

The residence nil-rate band applies only when you pass your main home to direct descendants, children or grandchildren. If your estate exceeds £2 million, this additional allowance tapers away by £1 for every £2 over the threshold. Many families assume they’re safe from inheritance tax, but frozen thresholds combined with property appreciation mean more estates now fall within taxable territory.

Agricultural and business property relief will be tightened from April 2026, with full relief capped at £1 million and only 50% relief thereafter. This change significantly impacts farming families and business owners who previously relied on unlimited relief to pass assets tax-free to the next generation. If you own farmland, business premises, or trading company shares, you need to review your estate structure immediately.

| Relief type | Current rule | New rule from April 2026 |

|---|---|---|

| Agricultural property | 100% relief, no cap | 100% relief up to £1m, then 50% |

| Business property | 100% relief, no cap | 100% relief up to £1m, then 50% |

| Residence nil-rate | £175,000 per person | £175,000 per person (frozen) |

| Standard nil-rate | £325,000 per person | £325,000 per person (frozen) |

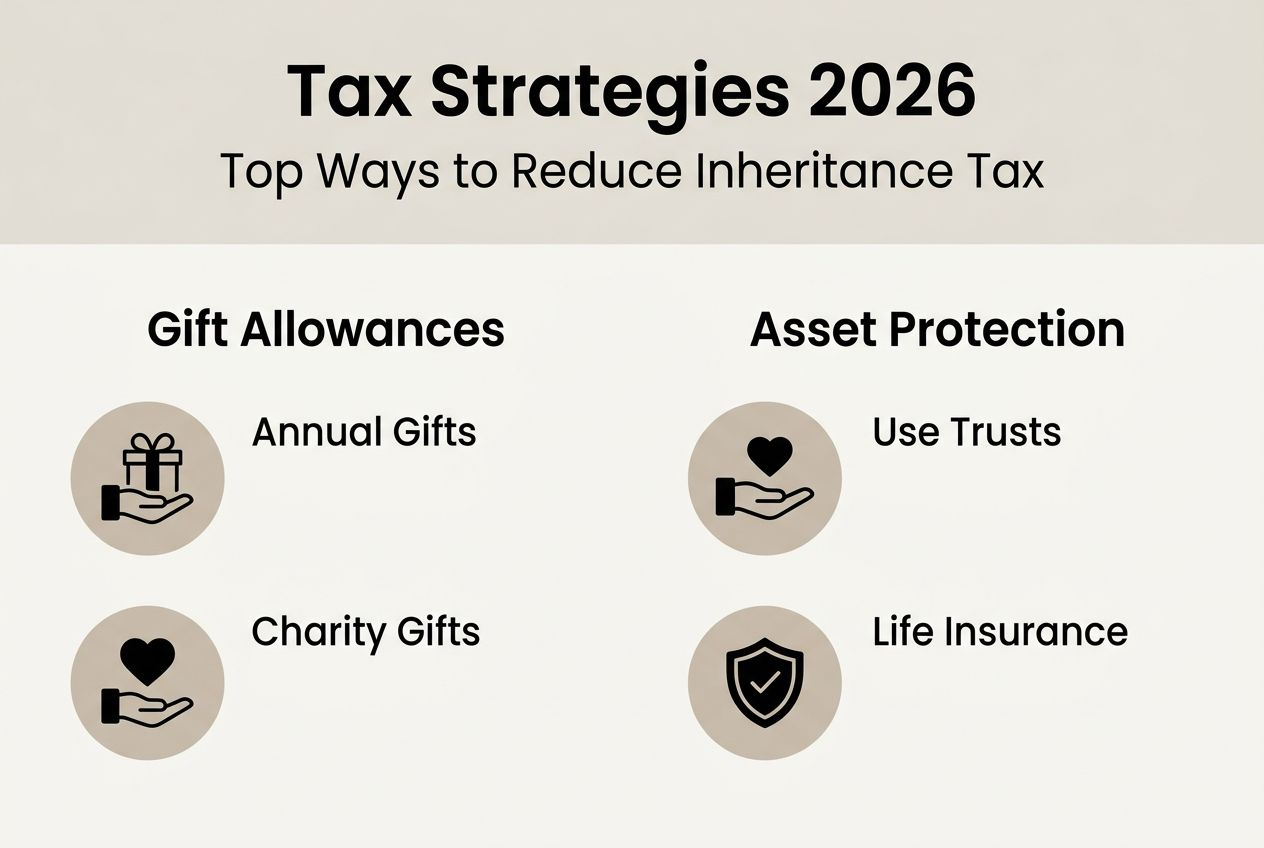

You can reduce your inheritance tax liability through several legal strategies. Annual gift exemptions allow you to give away £3,000 per year tax-free, with unused allowances carried forward one year. Gifts to spouses or civil partners are exempt, as are donations to registered charities. Potentially exempt transfers, gifts made more than seven years before death, fall outside your taxable estate entirely.

Consider using trusts to protect assets whilst retaining some control during your lifetime. Discretionary trusts, bare trusts, and interest in possession trusts each offer different benefits depending on your family circumstances and asset types. Life insurance policies written in trust pay out directly to beneficiaries without forming part of your taxable estate, providing immediate funds to cover inheritance tax bills without forcing property sales.

Pro Tip: Schedule a review with a specialist solicitor before April 2026 to restructure business and agricultural assets, maximising relief under current rules whilst preparing for the new caps.

Making a will that protects your assets and family

A legally sound will forms the foundation of effective estate planning. Without one, intestacy rules dictate who inherits your estate, often producing outcomes that contradict your wishes and leaving unmarried partners with no automatic rights. Caveat applications rose to 11,362 in 2024, a 79% increase since 2010, highlighting how poorly drafted wills invite expensive legal challenges that drain estate value and damage family relationships.

The UK recognises several types of wills, each serving different needs. Single wills suit individuals with straightforward estates, whilst mirror wills allow couples to create matching documents with reciprocal provisions. Property protection trusts preserve assets for children from previous relationships, preventing new partners from inheriting everything. Discretionary trusts give trustees flexibility to distribute assets based on beneficiaries’ changing circumstances.

Creating a valid will requires following strict legal formalities. You must be at least 18 years old and have mental capacity to understand the document’s effect. The will must be written, signed by you in the presence of two independent witnesses who also sign, and those witnesses cannot be beneficiaries or married to beneficiaries. Failure to meet these requirements renders the entire document invalid.

- Appoint executors who will administer your estate, ideally people you trust completely with financial and organisational skills.

- List all significant assets including property, investments, business interests, and valuable personal items with clear identification.

- Name guardians for children under 18, ensuring they’re willing to accept this responsibility before naming them.

- Specify beneficiaries and what each should receive, using percentages for residual estate to avoid mathematical errors.

- Include funeral wishes and organ donation preferences, though these aren’t legally binding on executors.

- Sign the document with two independent witnesses present simultaneously, ensuring all three sign the same page.

Digital assets represent a growing estate planning challenge. Your cryptocurrency wallets, social media accounts, online banking, cloud storage, and digital photo libraries all require specific planning. Without clear instructions and access credentials stored securely, executors cannot manage or distribute these assets. The proposed Wills Act 2025 aims to modernise the law, including recognising electronic wills and lowering the minimum age for creating a will, though paper wills remain the gold standard for now.

Create a separate digital assets inventory listing all online accounts, usernames, password manager details, and specific instructions for each platform. Appoint a digital executor, someone tech-savvy who understands these assets’ value and access requirements. Store this information securely but ensure your main executor knows how to access it when needed.

Pro Tip: Review and update your will every three to five years, or immediately after major life events like marriage, divorce, births, deaths, or significant asset acquisitions, as these can invalidate existing provisions.

Navigating the probate process effectively in the UK

Probate is the legal process that confirms your executor’s authority to administer your estate, collect assets, pay debts and taxes, and distribute inheritances according to your will. Not every estate requires formal probate, banks and financial institutions typically release funds under £5,000 to £50,000 without it, but most estates involving property or substantial assets need this legal validation.

Applying for probate follows a structured sequence that executors must complete carefully. Missing steps or submitting incorrect information causes delays that can stretch the process from months to years, particularly when beneficiaries need funds urgently.

- Locate the original will and register the death, obtaining multiple death certificates for different institutions.

- Value the entire estate comprehensively, including property, investments, bank accounts, personal possessions, and outstanding debts.

- Complete inheritance tax forms IHT205 or IHT400 depending on estate value, paying any tax due before probate issues.

- Submit probate application form PA1P with the original will, death certificate, and appropriate fee to the Probate Registry.

- Receive the grant of probate, typically within 8 to 12 weeks if no complications arise.

- Collect estate assets, settle outstanding debts and expenses, then distribute inheritances to beneficiaries as specified.

Probate timelines and costs vary significantly based on estate complexity. Simple estates with clear wills, cooperative beneficiaries, and straightforward assets might complete within six months. Complex estates involving business valuations, property sales, disputed wills, or international assets often take 12 to 18 months or longer.

| Cost element | Typical range | Notes |

|---|---|---|

| Probate application fee | £273 | For estates over £5,000 |

| Legal fees | £1,500 to £5,000+ | Varies with estate complexity |

| Property valuation | £200 to £500 | Required for accurate IHT returns |

| Estate administration | 2% to 5% of estate value | Professional executor fees |

Probate disputes have increased significantly, with common causes including ambiguous will wording, questions about testamentary capacity, allegations of undue influence, and family members excluded from inheritance. Prevent disputes by ensuring your will uses clear, unambiguous language, obtaining medical evidence of capacity if you’re elderly or unwell when making your will, and discussing your intentions with family members beforehand to manage expectations.

Dying without a valid will forces your estate through intestacy rules that follow a rigid legal formula. Your spouse receives the first £322,000 plus personal possessions and half the remaining estate, with children sharing the other half. If you have no spouse, children inherit everything equally. Unmarried partners receive nothing under intestacy, regardless of relationship length, making wills absolutely essential for cohabiting couples.

Pro Tip: Engage experienced probate solicitors early in the process to navigate complex valuations, tax calculations, and legal requirements efficiently, particularly for estates involving business interests or handling probate complications.

Estate planning for pension pots and digital assets in 2026

Pension planning takes on new urgency with upcoming tax changes. From April 2027, pension pots and death-in-service benefits will be included within IHT, ending decades of tax-advantaged wealth transfer. Currently, defined contribution pensions pass to nominated beneficiaries outside your estate, avoiding inheritance tax entirely. This significant advantage disappears in 2027, potentially adding hundreds of thousands of pounds to some families’ tax bills.

Review your pension beneficiary nominations immediately. Many people completed these forms decades ago and never updated them, meaning ex-spouses or deceased relatives remain listed whilst current partners or children are excluded. Pension scheme administrators pay death benefits according to these nominations, not your will, so outdated forms create serious problems.

Consider whether drawing pension income during retirement or preserving the fund for inheritance makes more sense under the new rules. Previously, leaving pensions untouched maximised tax-free inheritance. Now you might benefit from using pension funds for living expenses whilst preserving other assets that qualify for reliefs or exemptions. This calculation depends entirely on your individual circumstances, asset mix, and family needs.

Digital assets require specific estate planning attention because traditional legal frameworks weren’t designed for cryptocurrency, NFTs, digital media libraries, or online businesses. These assets can represent substantial value but become completely inaccessible without proper planning. Executors need detailed information about what digital assets exist, where they’re stored, and how to access them.

Create a comprehensive digital assets inventory covering:

- Cryptocurrency wallets with recovery phrases stored securely offline

- Online banking and investment platform credentials

- Social media accounts with instructions for memorialisation or deletion

- Cloud storage services containing important documents or photos

- Domain names and website hosting accounts

- Digital media purchases including ebooks, music, and films

- Online business assets like e-commerce stores or digital products

Appoint a digital executor, someone with technical knowledge who understands blockchain technology, cloud services, and digital security. This person should be different from your main executor unless they possess both legal and technical expertise. Provide clear written instructions for accessing each digital asset type, understanding that some platforms prohibit account transfers whilst others facilitate memorial accounts.

Store access credentials using a reputable password manager with a master password held by your digital executor. Never include passwords directly in your will, as wills become public documents after probate. Consider using a letter of wishes, a separate non-binding document that provides executors with practical guidance without becoming part of the public record.

Pro Tip: Review pension nominations and digital asset inventories annually, particularly after the pensions and divorce implications of any relationship changes, updating access credentials and beneficiary details to reflect current circumstances.

How Signature Law can support your estate planning journey

Estate planning involves complex legal requirements, tax calculations, and family considerations that benefit enormously from expert guidance. Signature Law’s specialist wills and probate solicitors provide personalised advice tailored to your unique circumstances, helping you navigate inheritance tax planning, will drafting, and probate administration with confidence and clarity.

Our experienced team, led by BBC and ITV-featured solicitor Sital Somaiya, combines technical legal expertise with genuine understanding of the emotional challenges families face during estate planning. We offer fixed-fee initial consultations, multilingual support, and compassionate guidance through every stage of protecting your family’s future.

Signature Law’s wills and probate services include:

- Bespoke will drafting incorporating tax planning and asset protection strategies

- Comprehensive probate administration handling all legal and financial requirements

- Inheritance tax advice addressing the 2026 and 2027 rule changes

- Trust creation and management for complex family situations

- Family law support when estate planning intersects with divorce or relationship breakdown

Don’t leave your family’s security to chance. Contact our family law solicitors in London today to start building a comprehensive estate plan that protects your assets, minimises tax liabilities, and ensures your wishes are honoured.

Frequently asked questions about estate planning in the UK

What happens if I die without a will in the UK?

Intestacy rules determine who inherits your estate according to a strict legal formula. Your spouse receives the first £322,000 plus personal possessions and half the remainder, with children sharing the other half. Unmarried partners inherit nothing regardless of relationship length, and the process typically takes longer and costs more than probate with a valid will.

How often should I update my will?

Review your will every three to five years as a minimum, and immediately after significant life events including marriage, divorce, births, deaths, or major asset changes. Marriage automatically revokes existing wills unless specifically made in contemplation of that marriage, whilst divorce revokes only provisions benefiting your ex-spouse.

Can I include digital assets in my will?

Yes, you should specifically address digital assets in your estate planning. Create a separate digital assets inventory with access instructions and appoint a digital executor with technical knowledge. Never include passwords directly in your will as it becomes a public document, instead use a secure password manager with the master password held by your digital executor.

What costs are involved in probate?

Probate application fees cost £273 for estates over £5,000, with legal fees typically ranging from £1,500 to £5,000 depending on complexity. Professional executor fees usually charge 2% to 5% of estate value, whilst property valuations cost £200 to £500. Complex estates involving business valuations or disputes incur significantly higher costs, making proper will planning essential to minimise expenses.

How will changes in 2026 affect my inheritance tax planning?

Agricultural and business property relief caps at £1 million from April 2026, with only 50% relief available above this threshold. From April 2027, pension pots and death-in-service benefits become subject to inheritance tax, ending their current exempt status. These changes require urgent estate plan reviews, particularly for farming families, business owners, and anyone with substantial pension wealth.

Should I use a solicitor or write my own will?

Whilst DIY will kits exist, solicitor-drafted wills provide legal certainty and reduce dispute risks. Professional advice ensures your will meets all legal formalities, uses clear unambiguous language, incorporates appropriate tax planning, and addresses complex situations like blended families or business assets. Probate costs from disputed or invalid DIY wills far exceed the expense of professional will drafting.

Recommended

- Types of Wills UK: 4 Key Options to Secure Your Family in 2026 | Signature Law

- Probate checklist UK 2026: essential guide to navigate probate | Signature Law

- Estate Planning in Divorce – Protecting Your Children | Signature Law

- Family disputes in probate explained: a UK legal guide 2026 | Signature Law